April 7, 2026

Energy Industry

Energy markets rarely move for a single reason. Prices respond to overlapping forces: global fuel supply dynamics, infrastructure constraints, weather patterns, and increasingly, geopolitical risk. In early 2026, several of these pressures are converging at once. For organizations managing energy costs, the result is a market environment that is becoming more complex and less predictable.

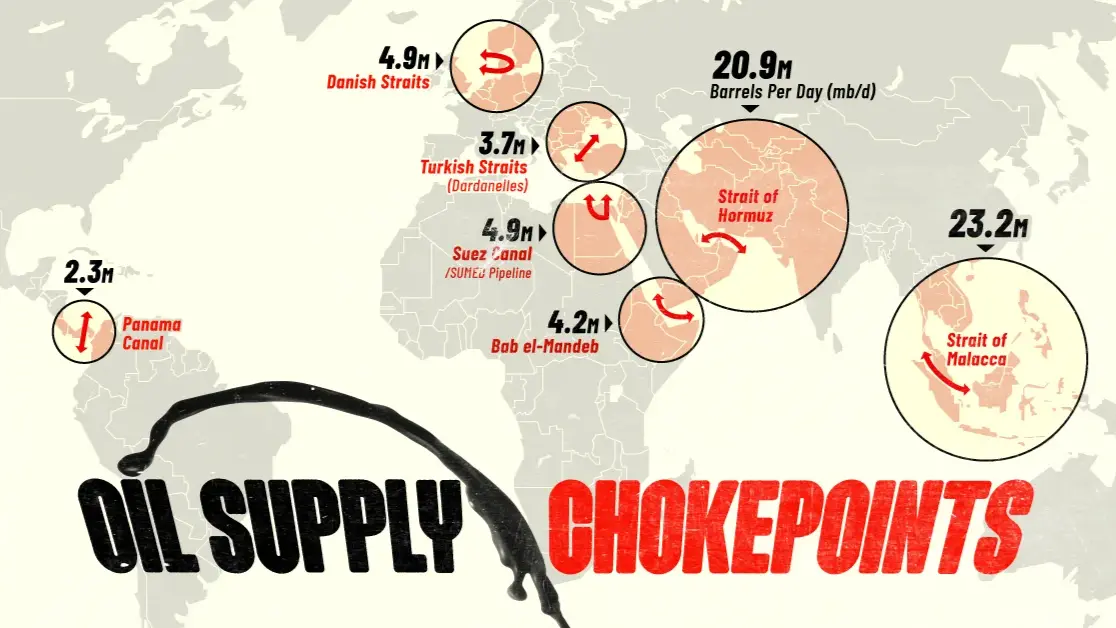

Recent geopolitical tensions in the Middle East have already begun influencing oil markets. Analysts surveyed by Reuters estimate that current geopolitical risks, particularly those involving Iran and the Strait of Hormuz, are adding roughly $4–$10 per barrel to crude oil price expectations for 2026. The adjustment reflects market risk pricing rather than immediate supply shortages, but it illustrates how quickly uncertainty can influence pricing outlooks (Reuters). Shipping risks are reinforcing that uncertainty. Security concerns affecting vessels traveling through the Red Sea have forced some oil and LNG shipments to take longer routes around southern Africa, increasing transportation times and pushing tanker freight costs higher.

The strategic importance of the Strait of Hormuz amplifies these concerns. Roughly 20% of global petroleum liquids consumption passes through this narrow corridor, making it one of the most important energy transit routes in the world. Even the possibility of disruption can quickly influence market expectations.

While these developments occur far from North America, the effects do not stay confined to oil markets. Energy systems are deeply interconnected, and price signals often travel across fuels.

Liquefied natural gas markets provide one example. Many LNG contracts are indexed to oil benchmarks, meaning movements in crude markets can gradually influence gas pricing structures. As LNG exports from the United States expand, global gas demand increasingly feeds back into North American markets. Natural gas already plays a central role in electricity generation. In the United States, natural gas accounted for roughly 43% of utility-scale electricity generation in 2023, which means changes in gas prices frequently translate into changes in power market pricing (EIA).

At the same time, electricity systems themselves are experiencing structural change. Demand for power is rising as economies electrify, new industries expand, and energy-intensive sectors such as data centres grow. These pressures are beginning to appear in capacity markets and long-term planning discussions across North America.

One signal of this shift came from the PJM Interconnection, the largest wholesale electricity market in the United States. Its most recent capacity auction for the 2026–2027 delivery year cleared at $329.17 per MW-day, significantly higher than previous auctions. Capacity markets are designed to ensure enough generation is available to meet future demand, and rising clearing prices often indicate tightening supply margins.

Electricity prices have also trended upward over the past decade. According to the U.S. Energy Information Administration, average residential electricity prices increased by approximately 32% between 2013 and 2023, reflecting a combination of fuel costs, infrastructure investment, and grid modernization.

Taken together, these developments highlight a broader shift in how energy risk is emerging.

Global geopolitical tensions can influence oil markets, oil price movements can shape LNG contracts, LNG trade can influence natural gas pricing, while natural gas markets often determine marginal electricity generation costs. At the same time, electricity systems themselves are adjusting to rising demand and infrastructure investment.

For organizations managing energy consumption, these dynamics mean energy costs are increasingly shaped by multiple interacting forces rather than a single market driver.

Understanding how those forces connect and monitoring them before they translate into price changes is becoming an important part of long-term energy planning.

For organizations managing energy costs, these signals are worth watching closely. Geopolitical risk, fuel market linkages, and evolving grid conditions are beginning to shape price expectations in ways that traditional forecasting models do not always capture. In this coming week, our team will be discussing these developments in more detail with clients in our upcoming webinar, including how geopolitical developments and market fundamentals may influence energy pricing outlooks for the remainder of 2026.

Status:

OG Link:

Notes:

.webp)